Key Insights:

- Binance US’s upcoming listing of Hyperliquid’s $HYPE token has already caused a 6% price surge for HYPE.

- Hyperliquid is gaining traction in DeFi and is beating competitors like dYdX in trading volume and open interest.

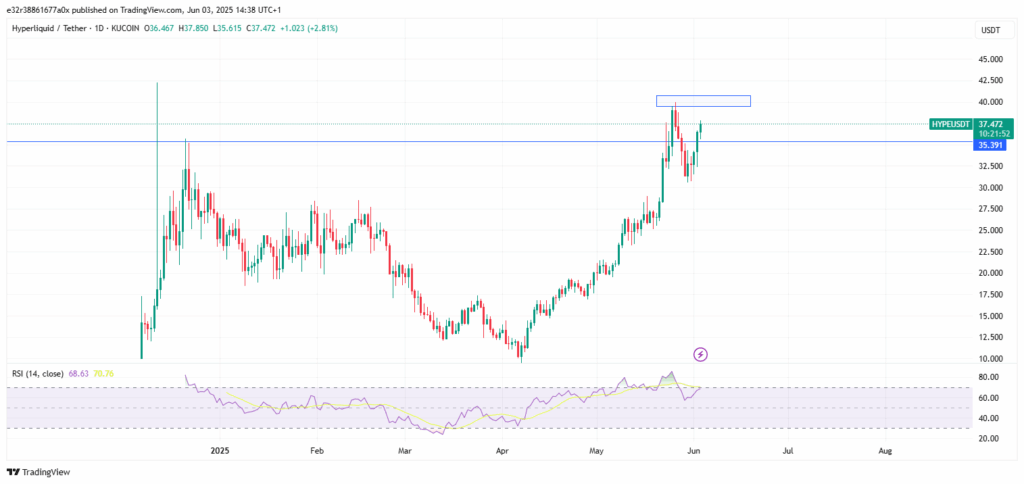

- Despite hitting the $39.96 high recently, $HYPE is facing resistance around $40 and the RSI on the daily chart shows that it could be overbought.

The crypto community has been buzzing with excitement throughout the week, especially after Binance US revealed plans to list the HYPE token.

The HYPE token is native to the Hyperliquid trading platform and while the announcement lacked a confirmed launch date, it has had some interesting effects so far.

So far, the price of HYPE has increased by over 6% within 24 hours. This stands as another major step forward for Hyperliquid, which has been gaining popularity on its own over the last few months.

A Bullish Signal With Sparse Details

On June 2, Binance US announced via social media that spot trading for HYPE would be “coming soon” to its platform.

Even though the exact date wasn’t part of the announcement, the statement was enough to generate excitement among traders and investors.

The listing is especially interesting, considering how Binance Futures had already introduced Perpetual futures contracts for HYPE only a few days before. However, the lack of specific timing has led to some cautious optimism.

Some in the crypto community are skeptical due to past tension between Hyperliquid and Binance. These concerns are coming from a recent incident involving the JELLYJELLY short squeeze crisis, in which Binance was accused of worsening Hyperliquid’s financial troubles.

There has been concrete evidence for these claims, but the episode has left a sense of mistrust among some users.

Hyperliquid’s Popularity in the Defi Space

So why is Hyperliquid so interesting as a platform?

The platform quickly became a force to be reckoned with in decentralized trading. The platform was built on its own layer-one blockchain and offers a low-fee trading experience that doesn’t rely on existing platforms like Ethereum or Solana.

This means that Hyperliquid has greater control over speed, scalability and user experience. As such, it is a very interesting alternative to centralized exchanges like Binance or Coinbase.

The platform quickly became a force to reckon with in decentralized trading. The platform was built on its own layer-one blockchain and offers a cheap trading experience that doesn’t rely on platforms like Ethereum or Solana.

This means that Hyperliquid has greater control over speed, scalability and user experience. As such, it is a very interesting alternative to centralized exchanges like Binance or Coinbase.

The platform recently set multiple records, including an all-time high in open interest at $10.1 billion as of May 26. Just days later, it overtook dYdX in trading volume and beat Sui in market cap.

These milestones were further improved by high-profile trades from crypto whale James Wynn, who helped popularize the platform and push its trading volumes to $8.6 billion.

Price Surge Incoming?

HYPE has shown considerable momentum in the market. After retesting its previous all-time high, the token surged to a new record of $39.96.

However, the rally was short-lived. Soon after this peak, HYPE pulled back for four consecutive days, which indicates that the $40 mark may now be a strong resistance level.

Indicators like the Relative Strength Index (RSI) indicate that the token may have entered an overbought phase.

This metric has hit a reading of 86.5 before retreating below its 14-day simple moving average (SMA), which could be a major sign of an incoming trend reversal. On the support side, the $28 to $30 price range appears to be important.

Historically, the $28 mark acted as a resistance level and could now flip to support. Traders are watching this area closely as a major pivot zone.

Intraday charts also show support around $31.5 and $30.5, with the next possible resistance target near $36 if the price rebounds.

Overall, the next few days could be very important for both Hyperliquid and its HYPE token. If Binance US provides an official listing date soon, it may inject more strength into the token’s price.

In a more general sense, Hyperliquid is setting itself up, not just as a trading platform, but as a major competitor to bigger platforms. Whether HYPE can stay above the $30 threshold and push beyond $40 depends on more than technicals.